Portfolio Update: Revisiting the “True North” in Our Approach

In this letter we share some thoughts from the Portfolio Managers at Broad Run Investment Management, LLC, the Fund’s sub-advisor.

-

David Rainey, CFACo-Portfolio Manager

David Rainey, CFACo-Portfolio Manager -

Brian Macauley, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio Manager -

Ira Rothberg, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Commentary

Last year, our more rate-sensitive holdings, including Brookfield Corporation, CarMax, NVR, RH, and Encore Capital, faced fundamental headwinds as they adjusted to a higher interest rate environment. This year, these stocks got off to a strong start with the expectation that a Federal Reserve easing cycle would kick off by mid-year. As inflation remains stubbornly elevated, that hope is now fading. While most of these stocks have reversed their early gains, their business fundamentals are looking up. Across the board, revenues have stabilized or expanded, with many showing margin improvement due to company specific initiatives. Regardless of the Federal Reserve’s timing, we believe these businesses are undervalued and positioned to lead the portfolio forward as their earnings growth returns to our expected mid-teens rate.

Our “True North”

We have had several years of difficult relative performance. While absolute returns have been reasonable, our portfolio has not been able to keep pace with the aggressive growth technology businesses that have driven outsized index performance over this period. This is disappointing, yet something we expect as an occasional consequence of our concentrated strategy focused on underappreciated, durable compounders. Outside of this period, our approach has delivered both solid absolute and relative returns over a long time.

At a moment like this, we believe it is helpful to step back and take measure of what we are trying to achieve and how we are trying to achieve it, to ensure we are on the right path.

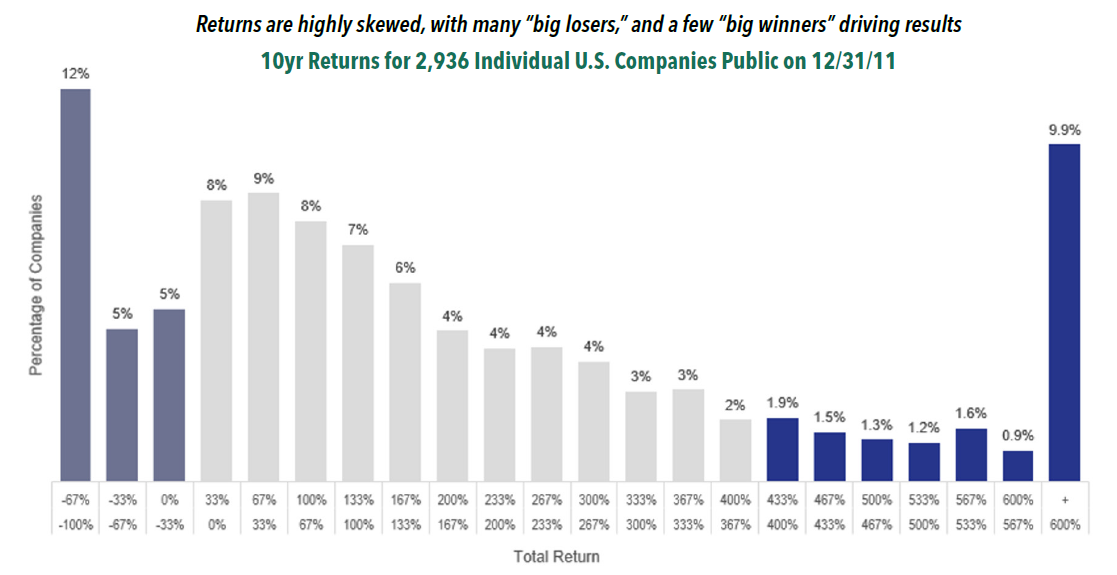

Market returns are driven by “right tail” outcomes, powered by businesses that compound at a high rate for an extended period of time. As economist Hendrik Bessembinder’s research has shown, just 3.4% of public companies have accounted for all value creation (in excess of risk-free Treasury Bills) over the last nearly 100 years1. Further, according to Bessembinder, 58.6% of public companies have created no value (in excess of risk-free Treasury Bills) over the duration of their public company lifetime.

Even over a shorter a period of time we can see this multimodal return pattern taking shape. We show on the chart below the distribution of stock returns over the decade ending 12/31/212 (the most recent period for which we complied data). While average returns are higher than long-term history (it was a decade of high equity market returns), the presence of significant right tail and left tail outcomes is evident.

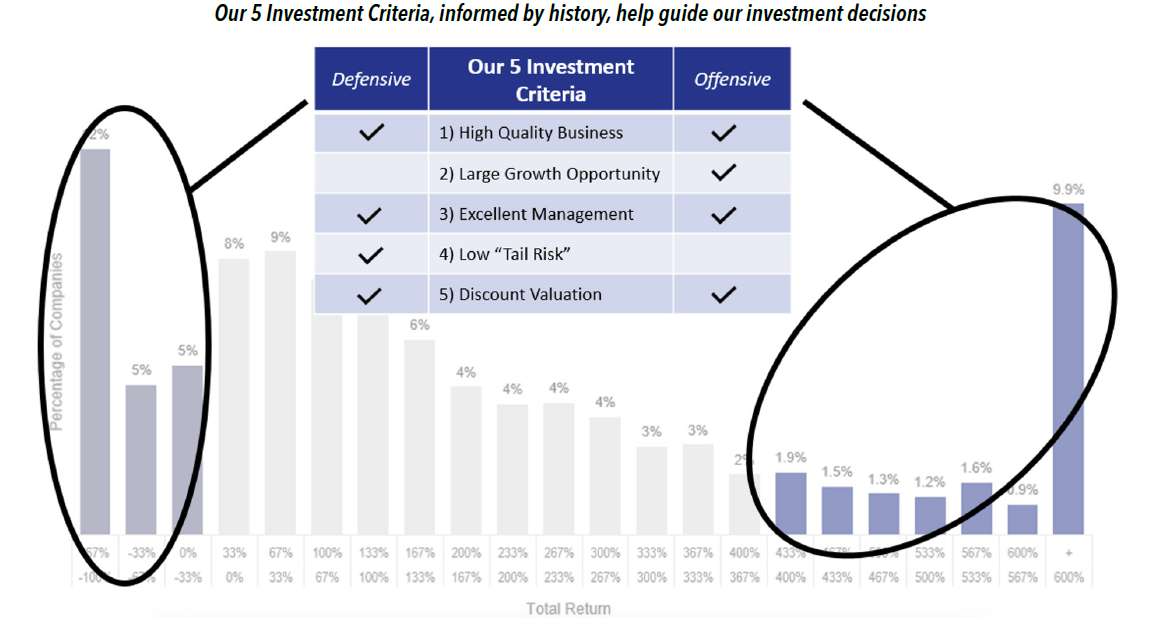

We have been working as a team to identify attractive investment opportunities for about 20 years. Throughout that time, we have employed an investment approach mindful of the market’s return distribution, designed to capture right tail outcomes while simultaneously avoiding left tail results. As overlayed below, our five investment criteria contain both offensive and defensive attributes to guide our investment decision making.

Our self-assessment is that we have been good at avoiding left tail outcomes. When we have had an investment end up there, our allocation was small in size, mitigating overall portfolio impact. We have also been reasonably successful at identifying and sizing positions that end up in the right quartile of outcomes, including a few breakout performers such as O’Reilly Automotive, Ashtead Group, and Aon. While only one of these businesses fell in the extreme right tail, we are confident we have a formula for finding other big winners over time. Indeed, we have several positions in the portfolio today that we think have 5x or 10x potential as we look out over the next decade.

One area we think we have opportunity for improvement is in avoiding investments that are “stuck in the middle.” These are businesses that are relatively mature, and entrenched in their industry, so unlikely to go backwards. But these companies also lack the ingredients for high rates of compounding that provide opportunity to land in the right tail. We have occasionally allowed such businesses to linger in our portfolio for too long because they were “safe and cheap,” but the opportunity cost has been high. We have exited a handful of these positions in recent quarters, and will be on heightened alert for their presence in our portfolio going forward.

Click here for a full listing of Holdings.

Click here for full, standardized Fund performance.

- In this article:

- Domestic Equity

- Focus Fund

You might also like

-

Portfolio Perspective

Portfolio Perspective

Cornerstone Large Growth FundHigh Profitability and Attractive Valuations – A Compelling Combination

Neil J. HennessyChief Market Strategist and Portfolio Manager

Neil J. HennessyChief Market Strategist and Portfolio Manager Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager L. Joshua Wein, CAIAPortfolio ManagerRead the Commentary

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Cornerstone Large Growth Fund discuss the Fund’s formula-based investment process and how it drives the Fund’s sector and industry positioning.

-

Portfolio Perspective

Portfolio Perspective

Cornerstone Value FundDriven by Revenues, Cash Flow, and High Dividend Yields

Neil J. HennessyChief Market Strategist and Portfolio Manager

Ryan C. Kelley, CFAChief Investment Officer and Portfolio Manager

L. Joshua Wein, CAIAPortfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Cornerstone Value Fund discuss the Fund’s formula-based investment strategy and how it drives the Fund’s sector and industry positioning.

-

Portfolio Perspective

Portfolio Perspective

Focus FundLong-term Investing in a Concentrated Collection of Businesses

David Rainey, CFACo-Portfolio Manager

Ira Rothberg, CFACo-Portfolio Manager

Brian Macauley, CFACo-Portfolio ManagerRead the CommentaryIn the following commentary, the Portfolio Managers of the Hennessy Focus Fund summarize the 2024 market and provide their insights on their 2025 outlook, including the impact on holdings from presidential administration’s policy changes and the growth of AI.